Calgary Tax Consulting provides professional non-resident tax consulting services across Calgary and Canada-wide, specializing in Part XIII withholding tax, Section 216 elections, and Certificate of Compliance filings. Our non-resident tax consultants handle NR4, NR6, and T2062 applications for Canadian expats, cross-border investors, and non-resident landlords navigating complex CRA obligations from outside Canada.

This Guide is meant for Non-Residents of Canada that own rental properties in Canada.

CRA imposes 25 percent Part XIII withholding tax on Canadian-source income paid to non-residents, including rental income, dividends, pension payments, and RRSP withdrawals, with a 10 percent late remittance penalty applied when withholding obligations get missed. A missed T2062 Certificate of Compliance filing before disposing Canadian property triggers 25 percent withholding on gross proceeds rather than the actual capital gain. Most non-residents discover these obligations after receiving CRA assessment notices demanding immediate payment of withholding taxes, penalties, and compounding daily arrears interest.

Our non-resident tax consultants in Calgary prevent these costly mistakes through proactive CRA compliance management. Your NR6 application gets filed before January 1st to reduce withholding from 25 percent on gross rental income to the net rental income amount, your Section 216 election recovers excess withholding tax, and your T2062 gets submitted within 10 days of property disposition. Non-resident landlords, cross-border investors, and Canadian expats all face the same risk without professional guidance, missing treaty-reduced rates that lower dividend withholding from 25 percent to 15 percent under the Canada-US tax treaty.

Our non-resident tax filing services in Calgary handle NR4 and NR6 preparation, Section 216 and Section 217 elections, T1243 deemed disposition calculations, and ITN applications through RC151 for non-residents without Canadian Social Insurance Numbers, managing your full CRA non-resident tax obligations year round.

The non-resident must withhold and remit non-resident tax at a rate of 25% of either the gross rental income amount (if no NR6 is prepared) or the net rental income amount (if an NR6 is approved by CRA).

The payer of the non-resident tax, which may be the tenant or property manager, must make the payment to CRA on or before the 15th day of the month following the month the rental income was paid.

The non-resident must set up a non-resident account number by calling CRA.

CRA may apply a penalty for a non-resident who fails to remit tax when:

| Days Late | Penalty |

|---|---|

| 1-3 | 3% |

| 4-5 | 5% |

| 6-7 | 7% |

| +7 or never remitted | 10% |

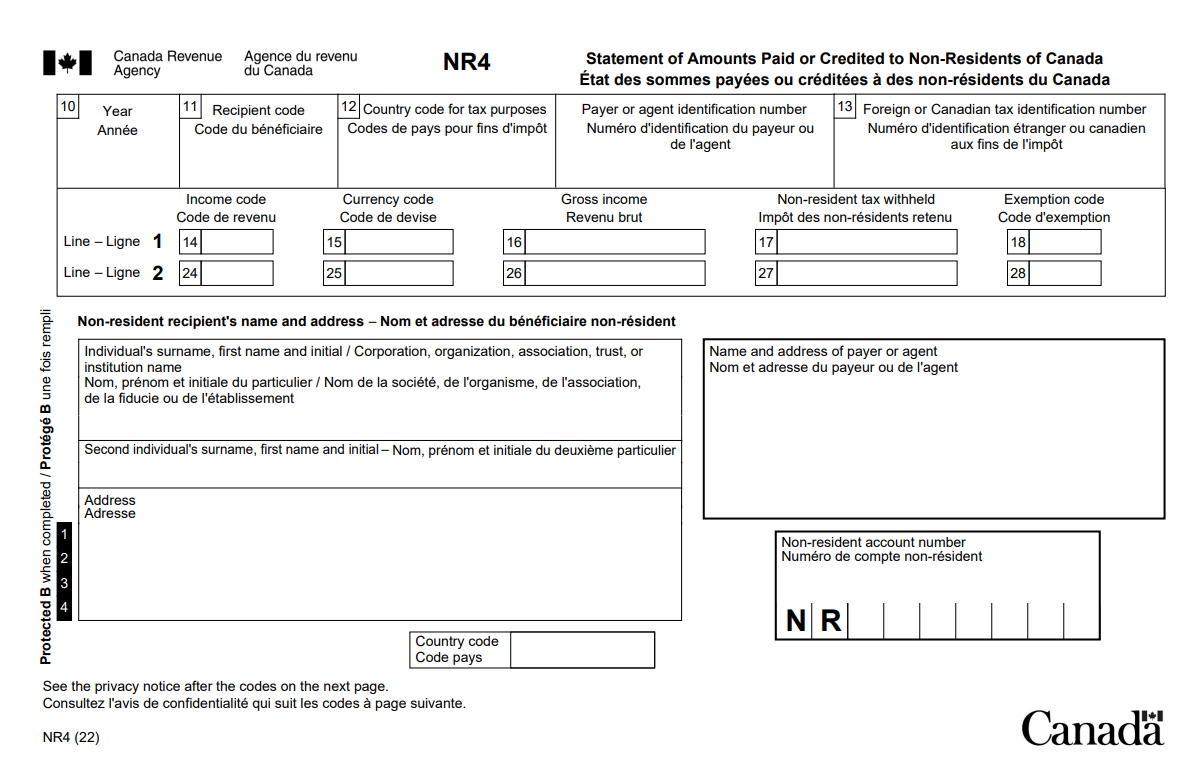

An NR4 slip must be attached to the back of your section 216 return.

The NR4 slip shows the gross rental income and non-resident tax withheld and remitted for the taxation year.

Note: If you are a co-owner (i.e. you and your spouse each own 50% of the rental property), an NR4 slip must be prepared for each co-owner and should reflect each co-owners share of the gross income and non-resident tax withheld.

The NR4 slip and summary must be submitted to CRA by March 31st.

If the NR4 slip and summary is filed late or never filed, CRA may assess a penalty of $100.

If you have an agent (i.e. a property manager) they typically prepare the NR4 slip.

However, if your agent did not prepare the NR4 slip, Calgary Tax Consulting can prepare it.

If a non-resident does not have an agent, then an NR4 Pro Forma must be prepared.

An NR4 Pro Forma is a letter sent to CRA requesting that CRA prepare the non-resident’s, NR4 slip.

The non-resident can prepare the NR4 Pro Forma or Calgary Tax Consulting can prepare it.

Information required for the NR4 Pro Forma:

The NR4 Pro Forma must be submitted to CRA by March 31st.

When filing the section 216 return, if we have not yet received the NR4 slip by CRA, we attach the NR4 Pro Forma to the section 216 return and request CRA to attach the slip to the return.

An NR6 allows the non-resident to withhold and remit non-resident tax at 25% of the net rental income amount instead of the gross rental income amount.

In order to file an NR6, the non-resident must appoint an individual to be their agent. The agent can be a property manager or another person such as a family member.

To prepare the NR6 form, the non-resident must provide an estimation of the expected gross rental income and expenses for the next tax year.

When submitting the NR6 form, a breakdown of the expected expenses must be attached.

The NR6 should be filed on or before January 1st of each year.

If an NR6 was approved the section 216 return is due on or before June 30th

If no NR6 was prepared or approved the section 216 return is due 2 years from the end of the year the rental income was paid to you.

If you disposed of the rental property and are including a recapture of the CCA you must file the section 216 return by April 30th.

The non-resident must notify CRA of the disposition of the rental property within 10 days from the date the property was disposed.

The non-resident must fill form T2062 http://www.cra-arc.gc.ca/E/pbg/tf/t2062/t2062-16e.pdf .

If you claimed CCA in prior section 216 returns and you disposed of the property, the section 216 return for the current period must include a recapture of the CCA.

If a terminal loss occurred as a result of the disposition, the loss must also be reported on line 126.

If a Calgary Tax Consulting is preparing the NR4 Slip, NR4 Pro Forma, NR6 or if you need a Calgary Tax Consulting to contact the CRA Non-Resident Withholding Department on your behalf. You must first authorize us by mailing an ORIGINAL signed NR 95 Form to following address as per CRA policy:

Non-Resident Withholding Section Sudbury Tax Centre

Sudbury ON P3A 5C1 Canada

Our Accountant will provide you instruction on how to fill out the NR95 Form.

Failure to fill form T2062 within 10 days after the date of disposition will result in a penalty of $25 a day.

If you have a balance owing you should pay it on or before April 30th.

Interest is charged for balance owing starting May 1st.

The non-resident must complete 2 documents:

If the non-resident would like to have an NR6 prepared they must fill an additional document:

| Form | Fee (Individual) | Fee (Joint) |

|---|---|---|

| Section 216 | $350 | $450 |

| NR4 Slip/NR4 Pro Forma | $100 | $150 |

| NR6 | $150 | $200 |

Let Calgary Tax Consulting experts file your belated return & claim your tax.

We go above and beyond standard withholding tax compliance and work with you to examine NR6 elections, Section 216 opportunities, and treaty-reduced rates. Non-resident rental income, pension payments, and investment returns are complex matters that require knowledgeable and experienced non-resident tax specialists.

At Calgary Tax Consulting, we align our non-resident tax strategies with your cross-border investment and income objectives. We are a team of professionals who focus on minimizing your Canadian withholding tax burden and maximizing wealth retention through strategic treaty applications.

EXCELLENTTrustindex verifies that the original source of the review is Google. Narinder and Sandeep are professional, knowledgeable, reliable, and fantastic to deal with! I use them for both my personal and business taxes, they make things easy and stress free. I would highly recommend them for exceptional accounting services!Posted on GoogleTrustindex verifies that the original source of the review is Google. I’ve been using the services at Calgary Tax Consulting for several years now, and I’ve always had a great experience. Their team is knowledgeable, prompt, punctual, and easy to deal with. The service is consistently excellent—I would highly recommend them.Posted on GoogleTrustindex verifies that the original source of the review is Google. Great experience with Calgary Tax Consulting. They were professional, knowledgeable, and explained everything clearly. The process was smooth and stress-free, and they were quick to respond to my questions. The price is worth it for the quality of service. Highly recommend.Posted on GoogleTrustindex verifies that the original source of the review is Google. Stay far away from Calgary Tax Consulting. They handled our taxes last year and made several massive errors that resulted in us owing the government over $2,000. Because of their negligence, our child benefits were withheld to cover the debt. To make matters worse, when we reached out via email to explain the situation and give them a chance to fix it, they completely ignored us. They are happy to take your money, but they won't stand by their work or even respond when they fail you. They charged us over $300 for 2 very basic tax filings.Posted on GoogleTrustindex verifies that the original source of the review is Google. Best accounting firm ever! Narinder and Sandeep are very professional and always helpful. We do our business taxes with them and couldn’t be happier. Great accountants in Calgary, highly recommended!Posted on GoogleTrustindex verifies that the original source of the review is Google. Best accounting firm ever! Narinder and Sandeep are extremely professional and knowledgeable. We do our business taxes with them, and they are excellent accountants. Highly recommend this firm to anyone in Calgary looking for reliable and trustworthy accounting services.Posted on GoogleTrustindex verifies that the original source of the review is Google. The members of Calgary Tax Consulting have truly made the tax process easy and simple. I have worked with them for over 10 years, it has been best decision I have made of my business with great results, thanks again to the entire team!Posted on GoogleTrustindex verifies that the original source of the review is Google. Narinder and his team are knowledgeable and helpful in navigating the complexities of the Canadian tax system.Posted on GoogleTrustindex verifies that the original source of the review is Google. I have used Calgary Tax Consulting for many years. They are always there to answer my questions, support me with documents and are always kind. I would highly recommend this team of professionals.Posted on GoogleTrustindex verifies that the original source of the review is Google. All of the staff are great, helpful, and stay on top of things. They have helped me and my business tremendously and I am looking forward to working with them for years to come.

Professional NR6 applications and Section 216 elections to reduce withholding tax from 25% gross rental income to net rental income calculations.

Expert T2062 Certificate of Compliance filings to minimize withholding tax on Canadian property dispositions and protect your capital gains position.

Strategic Part XIII withholding tax management with treaty-reduced rates, proper remittances, and CRA compliance to avoid penalties and arrears interest.

Complete non-resident tax return preparation with ITN applications, residency determinations, and cross-border tax planning for Canadian expats and investors.